UPDATE: Rules and forms referenced in this post were amended on December 1, 2017.

There is a difference between avoiding a lien under section 522(f) and treating a secured claim as wholly unsecured based on the value of the collateral. The latter is colloquially referred to as lien-stripping, but often it is erroneously considered a lien avoidance action, which causes confusion as to how the claim is to be treated in the plan.

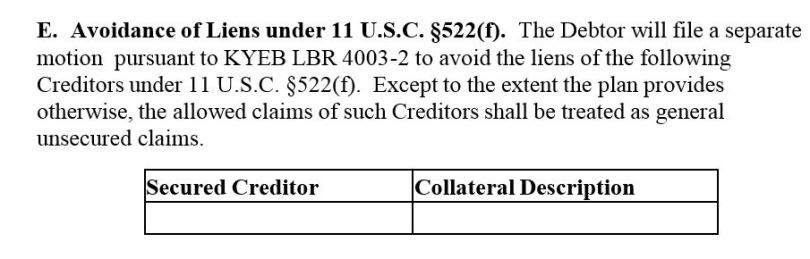

Lien Avoidance Under 11 U.S.C. § 522(f).

The debtor may use section 522(f) to avoid a lien –

- to the extent the lien impairs an exemption;

- and only if the lien is –

-

- a judicial lien (in Kentucky, judgment liens on real property); or

- a nonpossessory, nonpurchase-money security interest in household goods and other property described in 522(f)(1)(B).

Section 522(f)(2) sets forth the arithmetic formula for determining whether a lien impairs an exemption and can be avoided. The judgment lien does not necessarily have to be junior to all other non-avoidable liens.

In the EDKY, the form chapter 13 plan has a place for listing creditors whose liens are to be avoided under § 522(f) (Section II.E. of Local Form 3015-1). By listing the creditor in the plan, the claim will be treated as unsecured, but that does not actually avoid the lien. The debtor must file a separate motion and get an order avoiding the lien.

Local Rule 4003-2 requires very specific information to be included in the motion and in the order avoiding the lien. If it’s a judgment lien to be avoided, the motion must identify not only the creditor, but the filing date, county, book and page number of the judgment lien as well (which should make it easier to get the lien released after the debtor gets a discharge). The motion also needs to show the calculation required by section 522(f)(2) (in other words, you have to “show your math”).

Even if the information were not required by local rule, it’s a good practice to follow.

Lien Stripping.

The Code does not refer to cramdown, strip down, strip off, lien-stripping, or any other familiar, descriptive terminology, but these terms generally refer to the process of valuing the collateral under 11 U.S.C. § 506 to determine the amount of the creditor’s secured claim, then dealing with the claim accordingly in the chapter 13 plan (or appropriate motion).

Section 1322 provides that a plan may modify the rights of holders of secured claims (except a claim secured only by a security interest in real property that is the debtor’s residence) or of unsecured claims.

To determine the amount of an allowed secured claim, go to section 506(a)(1) (“Determination of Secured Status.”). An allowed claim is secured only to the extent of the value of the property to which the lien attaches; the remainder of the claim is considered unsecured. If there is a junior lien that is “underwater” – in other words, there is no value for the junior lien to attach to – it is entirely unsecured.

For example, property worth $100,000 is encumbered by a 1st mortgage in the amount of $120,000 and a 2nd mortgage of $10,000. There is no value in the property to which the 2nd mortgage can attach. It is a wholly unsecured claim under § 506(a).

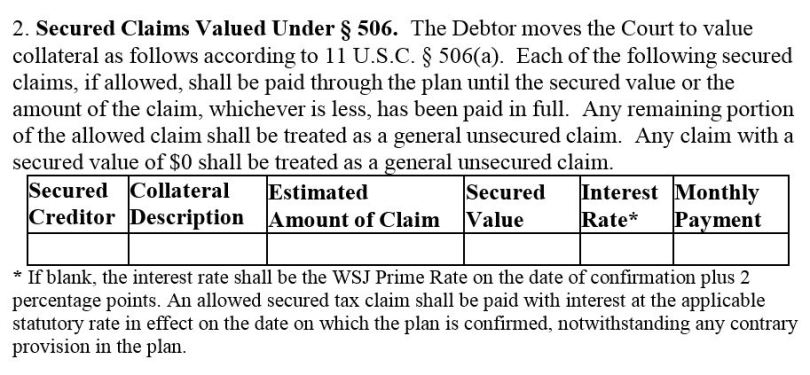

How should a claim be treated in the plan if there is no value in the collateral for the lien to attach to? Don’t make the mistake of listing it in the section on avoiding liens under 522(f). You are not using section 522(f) to avoid the lien. List it in the section of the plan called “Secured Claims Valued Under § 506” (which is Section II.A.2. of Local Form 3015-1).

What is the value of the secured claim of the lienholder who is totally underwater? $0. The claim is treated as wholly unsecured.

Here, we are talking about whether there is value in the property for a lien to attach to. The debtor’s exemption in the property plays no role in this analysis. Liens that can be stripped off could be second or third mortgages; second liens on cars; judgment liens on property that is already fully encumbered.

Creditors might argue that it takes an adversary proceeding to strip off a lien, and some courts have so held. Other courts require a separate motion to value collateral and strip off a lien (WDKY). In the EDKY, the plan provision for valuing collateral constitutes a motion, and the lien can be stripped through plan confirmation.

Treating the claim as unsecured in the plan does not necessarily get the lien released at the conclusion of the case. There is no federal or local rule describing how to actually make the lien go away after the debtor gets a discharge. A well-crafted plan or motion will contain language in the Special Provisions section that requires the creditor to file a release of its lien within x days after the debtor’s discharge is entered.

In a future post, I’ll discuss what happens when a lien is not properly perfected, or is perfected during the 90-day prepetition period, or is perfected postpetition. In those instances, the trustee (and in some instances the debtor either directly or derivatively) has the power to avoid transfers, including the granting of a security interest or the perfection of a lien.

Make sure you understand the difference between avoiding a lien under 522(f) and treating the secured claim as unsecured because of the collateral’s value. Use the proper plan provision. File the appropriate motions and tender clear, direct orders. Give good notice to creditors. Then at the end of the case, make sure the affected creditors release their liens.

Really concise Beverly as this topic can and often does confuse some people. I’m sure this will help some of the newer Chapter 13 filers and it never hurts the rest of us to have a ‘refresher’ now and then.

LikeLike

Great information, as always. I particularly noted the suggestion to include a Special Plan Provision that details a release of lien. Thank you!

LikeLike